http://theconversation.com/factcheck-do-australian-banks-have-double-the-return-on-equity-of-banks-in-other-developed-economies-77784

http://www.uq.edu.au/economics/johnquiggin/JournalArticles01/CBAPrivatisation01.html

https://www.greenleft.org.au/content/new-call-%E2%80%98people%E2%80%99s-bank%E2%80%99-challenge-big-four

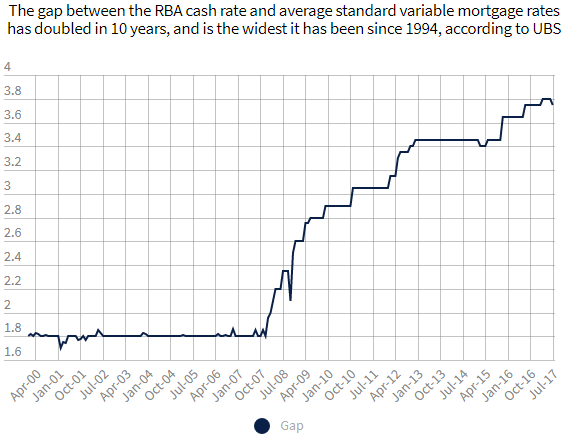

The difference between RBA cash rate and home loan rate used to be less than 1.8% in the 1980s 1990s and 2000s, now the difference is 3.75%:

Australia big four banks — the Commonwealth Bank, NAB, ANZ and Westpac — are together the most concentrated and profitable set of banks in the world.

Treasurer Scott Morrison was quoted on ABC Insiders, May 14, 2017:

"The banks in Australia have a return on equity which is about twice, if not more than that, what you see particularly in other parts of the advanced developed economies of the world."

A broader ROE comparison from research group Morningstar shows that Aussie banks’ 14 per cent ROE last financial year dwarfed the profitability of banks in Europe (4.7%) and Britain (1.7%), and was higher than the US, Singapore, China, Hong Kong and Switzerland:

- Canada 14.6%

- Australia 14%

- China 13.5%

- Singapore 9.8%

- USA 9.5%

- Hong Kong 8.7%

- Europe 4.7%

- Switzerland 3.9%

- Britain 1.7%

The big four banks are enjoying an implicit taxpayer subsidy worth almost $4 billion because their creditors know they will be bailed out in a crisis, new Reserve Bank research shows. In the first valuation of the subsidy by an Australian regulatory body, documents released by the RBA show that in 2013 the “total subsidy” to ANZ, Westpac, National Australia Bank and Commonwealth Bank was between $1.9bn and $3.75bn. The Reserve Bank has concluded that “the major banks have received an unexplained funding advantage over smaller Australian banks of around 20 to 40 basis points on average since 2000”.

The banks are also ripping off their customers with extortionate account-keeping fees and interest on bank cards. They also keep their interest rates on savings accounts at a minimal level, way below the rate they charge for housing and other loans.

The big banks often argue that much of their exorbitant profits ends up going back to ordinary citizens through their ownership of shares. In reality, more than 90% of Australians do not own shares directly, and for superannuation holders, the yearly gain will be only $142. This compares with the average $1460 annual profit for every person in Australia that the Big Four banks make through their retail operations alone.

If Australians paid less interest, say five grand less on their mortgages and spent it in the local shops it would deliver far greater economic benefits to the general Australian economy than most other measures. Too much money is going to the banks stifling the economic growth of the whole country.

Yet there is a very simply solution to this. Create a competitive banking environment through regulation and if that does not work simple create a new government owned bank where any profits go back to the Australian community.

Australia's largest bank, the Commonwealth bank started in 1911 as a Australian government owned bank and was fully privatised in 1996. To create a competitive banking environment the Australian government could simply create a new bank say Commowealth Bank 2 with the following features:

- Online and call centre only, no branches network

- Home loan interest rate: Reserve bank cash rate + 2%

- Eligible customers:

- Customer with existing home loan, never missed payments in 3 years

- Customer with LVR up to 70%, Income proof from ATO tax returns with max 30% to service the regular repayments

- Any profits go back to the Australian community.

Such an example of the state-owned bank is KiwiBank in New Zealand, run by the NZ Post Office. A similar operation in Australia would boost competition.

No comments:

Post a Comment